COVID changed the way many tech employees work. The option for remote work changed the way many of you think about life and what you want out of life. Instead of waiting until financial independence, or worrying about job opportunities in the new location, you can move to the place you really want to be! For others, many tech firms are moving to second-tier less expensive tech hubs like Tesla moving to Texas.

That might be near family, towards a dream home, or maybe closer to nature and a community you value. What an absolute blessing!

You may take a 10% pay cut from your current employer, but what you get is worth far more than that. Now it comes down to the logistics.

Many of our clients moved in the last year to smaller tech hubs. This allows them freedom of time and money – to be close to family and friends, buy a place to call home, or to just explore a different environment. During this tax season, we found that a few clients are already receiving Requests for Information from the state they moved from. This can be a bit daunting, so we want to share best practices and things to be aware of.

What do the states ask for in a tax request for more information?

Each state can be a bit different in the request, but the goal is to understand whether you are truly a resident or nonresident for tax purposes. They may ask for:

– Official date you changed your status from resident to nonresident

– Documentation that supports this like

- Rental agreement / home purchase documentation

- Drivers license with date of issue

- Voting registration

- Updated insurance coverage and established health care in the current location

- Offer letter displaying the new location and start date

– Whether you traveled to the state during the year and specific dates of travel

- How many of those days were non-working days

- How many of those days were working days

- Whether you worked remote or in an office locally

The state’s intent is to ensure that income is appropriately allocated from your employment in the state. They are not trying to rob you of hard earned money, even though it can feel that way when you do not know the rules.

How can you prepare for your move to make this easier?

- Alert your HR department for the exact date you plan to leave your state fully. Waiting a month or two to update this may mean more income allocated and additional stock compensation accrued to that state on your W-2.

- Track your days/time spent visiting in your prior state once you move.

- Make it 100% clear where you are. I know it’s a jumble to move across the country (I’ve done it a few times myself), but the longer you wait to establish your presence, the less of an audit trail you have supporting your new move.

- Remember that your RSUs or stock options will still have a trail of income allocable to your prior state. Until the stock is recognized as compensation income, you technically earned a piece in your prior state. So even after you leave a state, there is a high likelihood that your next vesting or option purchase will show the allocation back to your prior home.

Moving between states is hard enough. Between packing, shipping, temporary housing, etc there are a million balls in the air. I hope the above information helps you prioritize which ball to catch a bit faster.

The above discussion is for informational purposes only. Recommendations are of a general nature, not based on knowledge of any individual’s specific needs or circumstances, and there is no intent to provide individual investment advisory, supervisory or management services.

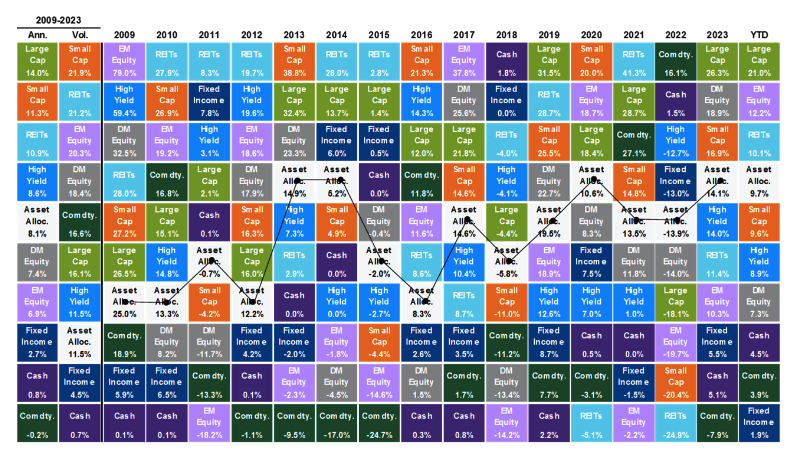

JP Morgan returns from JP Morgan Quarterly Market Review, Q3 2024

JP Morgan returns from JP Morgan Quarterly Market Review, Q3 2024