If you receive a large grant of RSUs or company stock, you will have many risks. Risk of termination before vesting, risk of market volatility in stock price, and asset concentration are a few. You will need to decide whether you will keep the stock once vested, or if you prefer to sell the stock at vesting date.

Concentrated Positions

A concentrated position occurs when you have a large amount of your finances wrapped up in one company. This can cause problems by increasing risk in your portfolio, causing tax issues, and liquidity needs. These risks compound if you have a long time horizon for your investment or your tolerance for risk in your financial plan is different.

Holding onto your company stock can leave you very dependent on one company’s success.

Chances are your salary, your 401(k) match, and your stock compensation are all tied to one company. This one company can ‘make or break’ your future financial freedom based on how well they do.

Example: If a competing product comes out, this may drop your stock value and require lay-offs longer term. Many smaller tech companies realize this pain when Amazon or Google announce a competing tool. The stock can plummet by 50% within a week.

Example: If a company ends up like Enron or WorldCom, then the drop may even be worse – wiping out your earnings and stock value completely. It may be hard to think this could be your company when we tend to be overconfident when we have an insider perspective on our employer’s prospects.

In these price drop scenarios, you may have paid significant taxes on the vested stock already as well.

On the flip side, if you hold on to the shares and the company goes gangbusters, you may also have significant capital gains accruing. Selling the entire position may not be tax-efficient and cause you a different headache.

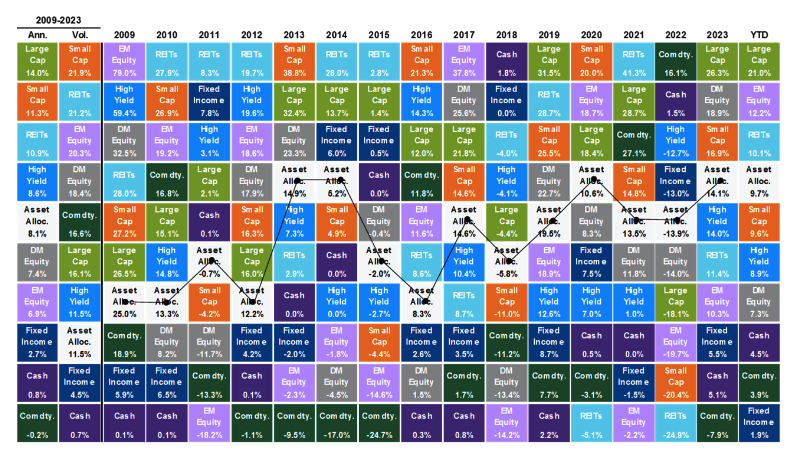

Diversification

Holding a large position in one company stock exposes you to higher risk of large movements in the stock price from day to day. Diversification is used to help investors choose a portfolio that offers the best return for a given level of risk. Why take on more risk than is necessary to achieve a given level of return?

A diversified portfolio is based on academic research into the disciplines of economics and finance. Research holds that investing in many different asset classes (i.e. emerging markets, U.S. large cap funds, etc) and in many companies within an asset class will reduce your investment risk. This seeks to avoid damaging investment performance by the poor performance of a single company stock or asset class.

At SeedSafe Financial we practice diversification for long term success. Find out more about our investment management services and consider giving us a call.

Find out how diversified your portfolio is through our free online tool.

Did you enjoy this post? Sign Up for my newsletter so you won’t miss another article.

JP Morgan returns from JP Morgan Quarterly Market Review, Q3 2024

JP Morgan returns from JP Morgan Quarterly Market Review, Q3 2024