Double trigger RSUs are a popular type of stock compensation leading up to an IPO. They are better for the employer – who doesn’t need to recognize stock expenses until IPO. They are less mental energy for the employee – who doesn’t have to pay taxes or make sell decisions until IPO.

What is the difference between single-trigger and double trigger RSUs?

RSUs are Restricted Stock Units your company gives you as an incentive to build company value.

The ‘single trigger’ versus ‘double trigger’ translates to 1 requirement or 2 requirements to ‘trigger’ vesting.

Single trigger vesting is generally based on ratable vesting over a period of time during employment (‘Service Vesting’). Double trigger RSUs include another vesting component.

If you have single trigger RSUs, check out our RSUs Basics blog post.

How does double trigger vesting work?

Double trigger RSUs are service vested (first trigger) and release at an IPO/exit (second trigger). When one unit meets both of these triggers, it vests to you and you receive one share of company stock.

Double trigger RSUs are different from stock options because there is no ‘option to buy’ the stock. Instead of having an option, your RSU immediately vests into stock when both triggers are met. At that point, you make the decision when to sell it.

What happens to a double trigger RSU at an IPO?

Double trigger RSUs are generally taxable as ordinary income (like your salary) at IPO.

The income and tax withheld (federal and state) at vest will be on your IRS Form W-2 from the company in the vesting year.

Since you pay income taxes on the vesting amount, this becomes your new ‘cost basis’. Each Custodian accounts for this a little differently on tax forms. Some adjust it on the 1099 and others provide a supplemental form that shows the true gain/loss on sales.

This is why maintaining your trade confirmations or statements from the custodian (i.e. Schwab, Shareworks, etc) is important.

If you miss those details on the supplemental form, then you could be paying doubled up taxes. If you know about how much vested, then you will know whether the 1099 looks right.

Does my company pay my taxes on the double trigger RSUs at vest?

Some employees are surprised when 40%+ of their vested shares sell for tax withholding purposes. Others end up with a surprise when they owe the IRS money on their tax return!

This happens because tax withholding ≠ tax due. Stock compensation is withheld at only 22% federally on the first $1M in stock/bonuses. This may differ from your actual effective tax rate in the end. If your effective tax rate is higher than 22%, be sure to set aside a higher percentage to help fund the tax bill.

At a state level, this can vary. Some states have a flat income tax, while other states (like California) have a different withholding rate from the tax rate. This means you may owe more taxes at a state level as well.

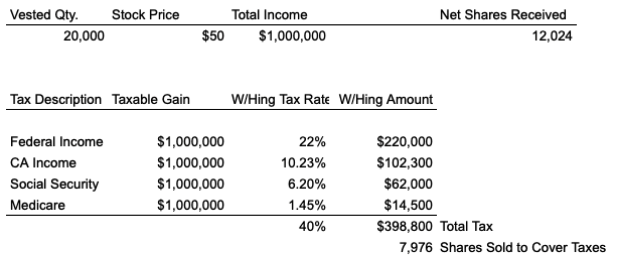

What is an example of taxes on a double trigger RSU?

Here’s an example of what it might look like.

40% of the shares sold for tax purposes, but this may not be enough withheld for Federal taxes if the individual makes over $1,000,000 in total. They may need to be ready to pay 10% or more ($100,000+) in taxes towards these shares on their tax return too.

When double trigger RSUs vest, you will want to make sure you account for this as you decide what to do with the shares.

Do I owe taxes on my double trigger RSUs if I hold onto them after the IPO?

If you decide to hold onto your shares after vesting, your stock will be like other stock investments.

If you decide to hold onto them, your holding period will start the day the shares vested to you and capital gains/losses will apply based on that date.

As a reminder: since you already paid ordinary income taxes on the value at vesting, your basis will be the fair market value from your vest date.

Do I owe taxes on my double trigger RSUs if I sell them after IPO?

After vesting, the stock is treated like any other stock investment. Capital gains/losses apply.

The type of capital gains tax is based on the length of time you hold the shares from the vesting date as well. Long term capital gains rates apply when you hold the stock more than one year from the vesting date.

After vesting, the swings in the stock price will count towards capital gains /losses on your tax return. This means you may owe more taxes on sale (if the stock appreciates beyond the vest value). If the stock loses value, you will not be able to offset the vesting income with the losses. Those losses are considered capital losses that can only offset other capital gains.

Example: Using the above example, your basis in the shares would be $1,000,000. If you sold the shares for $1,500,000 at a later date, you would be subject to capital gains tax on $500,000.

Depending on the time held, you would pay short term or long term capital gains tax (and the net investment income tax above a certain income level).

If you hold the stock and the price drops below the value at vesting, you may recognize a capital loss. You may be able to use those losses to offset capital gains from your company stock. Losses greater than current capital gains offset income up to $3,000 a year. Any unused losses carry forward to future years. Unfortunately, you can not claim the taxes paid at vesting back. This is one risk of many encountered in holding your company stock long term.

Following with the above example, if your basis in the shares is $1,000,000 and you sold the shares for $750,000 at a later date, you would have a loss of $250,000. Depending on other investment sales and capital gain distributions, you may be able to offset some of this loss or not. If you do not have any, you would only be able to claim $3,000 of capital gains loss on your tax return. The remaining $247,000 loss would carry forward to future tax returns.

This is where having an investment manager who can help you with gain harvesting may come into play. Check out our blog post on Do I need an investment manager? as well.

What happens to a double trigger RSU if you leave?

This will depend on the specific plan document for your company.

Generally, most double trigger RSUs are like regular RSUs at termination:

- If you have double trigger RSUs that are not time vested, those will expire immediately.

- If you have double trigger RSUs that did meet the time vesting component, it may depend more on whether termination was ‘for Cause’.

- In this case, ‘for Cause’ termination may result in complete termination. ‘Not for Cause’ termination is gentler and usually allows you to be eligible for the time vested RSUs to vest at IPO or exit.

This can be a bit more complicated tax-wise as well if you leave the state you were working in as the RSUs ‘Service vested’ too.

SeedSafe has worked with IPOing tech professionals since 2016 and we’ve gone through this many times. You may only experience it once, but the outcomes can be life changing. Our goal is to empower you with clarity and understanding of the process and outcomes.

We recommend all IPOing employees to bring on a financial advisor during the process to make sure nothing falls through the cracks. If you are looking for a financial advisor and tax advisor to help you through the process, please reach out to us.

Interested in learning more? Sign up for our newsletter

The above discussion is for informational purposes only. Recommendations are of a general nature, not based on knowledge of any individual’s specific needs or circumstances, and there is no intent to provide individual investment advisory, supervisory or management services.