Benefits enrollment season is upon us again and we often review if a HDHP or PPO makes more sense…it depends!

What health insurance is best for you depends on a few things:

- Your current health and how often you see a doctor,

- Whether you have extra cash to pay for medical costs, and

- If you feel you can emotionally take that risk

What are the terms to know when evaluating a HDHP vs PPO?

PPO – a ‘preferred provider organization’ gives you more in-network options for providers (doctors, medical offices, etc) than other plans may have. You also do not need a referral from your primary doctor for most specialists.

HDHP – a ‘high deductible health plan’ can actually be a PPO – the main difference is that it meets certain IRS requirements to qualify for adding an HSA ‘health savings account’. These plans typically have lower premiums but higher out-of-pocket costs.

Deductible – The cash you put towards doctors visits, prescriptions, etc before your health insurance pays the provider in full.

For PPOs, there is often a per visit and per medication amount you pay (‘copay’) up to the total deductible amount

For HDHPs, you generally pay the full cost of visits, care, and prescriptions until you reach the total deductible

Out-of-pocket maximum – the amount you pay before the health insurance company covers additional needs. Each insurance plan is different. The out-of-pocket amount is higher than the deductible and includes additional prescription payments, hospital visits, etc up to a certain dollar amount.

Premiums – your contribution from your paychecks to your health insurance plan

In-network vs out-of-network – In-network services are at a negotiated price with the health insurance plan. Out-of-network providers do not have a contract with the health insurance plan. Your out-of-network maximum cash out-of-pocket amount is generally much higher.

Is it better to have a PPO or HDHP?

This depends on your plans available. Review your summary of benefits in your enrollment package to understand insurer choices, premium cost, deductible, and out-of-pocket maximum.

Then, review each type of care listed to understand how the PPO or HDHP may cover each of those needs. Often you will see a lower copay and deductible for PPO plans but a higher premium.

The basic trade off is: a higher premium means lower costs for each care need. A lower premium means a higher out-of-pocket contribution.

So why would you choose a lower premium?

One reason may be if you are in good health and rarely see a doctor. You may choose to take the risk of not paying for health care services if you believe you won’t need many.

For higher-income earners, the reason may be to participate in the HSA ‘health savings account’.

What is a HSA ‘health savings account’?

An HSA ‘health savings account’ allows you to make pre-tax contributions to an account and make tax-free distributions from it to pay for qualified health insurance costs. What you do not use within the year will continue to remain in the account for future use. This beneficial treatment is limited to $8,300 for a family/$4,150 for an individual in 2024. For employees over age 55, there is an additional $1,000 catch up contribution available.

For high-income earners, this may mean saving 37%+payroll taxes on contributions to an HSA account or ±$3,500 a year! *Note, states like California may add the HSA back to taxable income. Federal, it will be a pre-tax benefit

What makes HSA accounts even more attractive is when an employer makes a contribution (free money!) or you are able to allow the HSA contributions to accumulate in the account. Most HSA accounts allow you to further invest what is in your account. This means these investments can continue to grow over time for future needs.

We know an HSA account allows tax-free distributions for qualified medical costs. It can also grow until you reach 59 ½+, then it can also be used for retirement expenses like an IRA or 401(k).

This makes the HSA account a triple threat for high income earners:

- A current pre-tax contribution

- Ability to pay for qualified medical costs tax-free, and

- Grow the account with investments long term for retirement

What is an FSA ‘flexible spending account’?

An FSA is another account that allows you to make pre-tax contributions for medical expenses you may have in a given year. This account is generally paired with the PPO and is limited to $3,050 in contributions in 2024. The downside is, if you don’t use it, you lose it! So you may decide not to max out this account and only put in what you believe you will need for the year. Some companies allow a grace period into the following year – but not longer than the first 3 months.

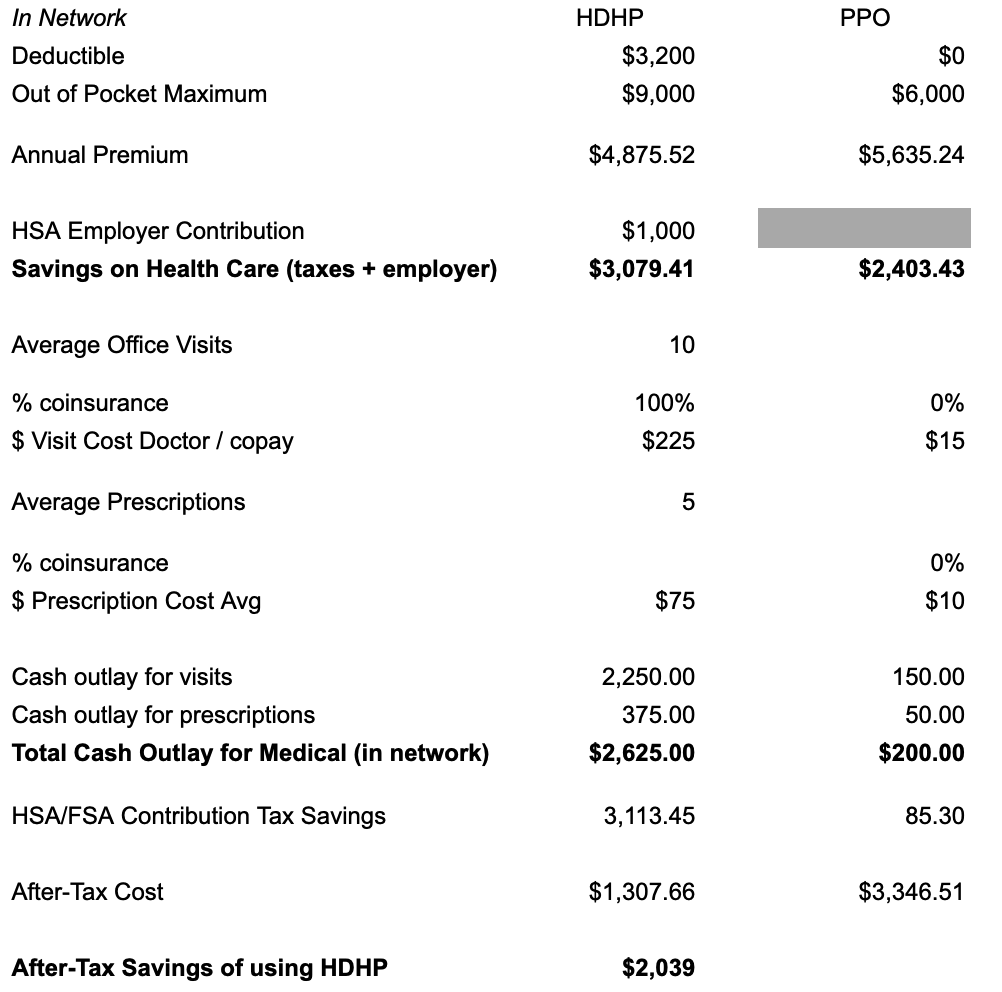

Example of a PPO vs HDHP

Annually, we do a review of our clients’ enrollment benefits to understand what is changing and review the available options. This tends to include an analysis of whether a PPO or HDHP may make more sense for them.

Let’s use the example of a family at the 35% tax bracket in income and the employee is 47 years old. They have excess cash above their expenses each month to use towards medical expenses and maximizing a contribution to an HSA. Their company provides a $1,000 family contribution to the HSA account. At this point, they tend to go to the doctor around 10 times a year and need a few prescriptions as things pop up.

First, we gather information on their deductible, out-of-pocket maximum, and premiums. Then, we talk through available health insurers and whether their current doctors would be considered in-network. If we feel pretty good about the information given, we will create a calculation to understand what the net after-tax cost of each option may be.

In this example we are looking at the tax savings and cash outlays of what are involved under each situation. The actual calculation for you may be very different, but in this example the HDHP means a current year benefit of $2,039 for the family.

This doesn’t include any long-term growth of allowing the HSA contribution to be invested and untouched for 12+ years.

When does a HDHP not make sense?

There is still a risk that your medical care needs are greater than expected or that you need out-of-network health care. If you travel often and enjoy riskier activities, then that may mean a higher likelihood that the savings of a HDHP do not materialize for you.

It also may not make sense if you do not have the cash available to maximize the HSA and pay for your medical expenses out of pocket.

Reviewing your benefits package is about making your best assessment. You can always change your mind with the next enrollment season 🙂

Did you enjoy reading this article? Join our newsletter to be notified when new posts are available.

The above discussion is for informational purposes only. Recommendations are of a general nature, not based on knowledge of any individual’s specific needs or circumstances, and there is no intent to provide individual investment advisory, supervisory or management services.