If you have double trigger RSUs and an IPO coming up, you may receive a ‘tax election’ from your company. This tax election allows you to decide how much you want to have set aside for taxes on your vesting RSUs at the time of IPO.

For the purposes of this conversation, we will hit on why you might want to choose one tax withholding option over another.

Why do I need to make a tax election at an IPO?

Remember, tax withholding ≠ taxes due. Tax withholding is a required high-level estimate of taxes that needs to be paid into the IRS throughout the year. Even if it feels like you’ve paid a lot in tax withholding, you may still owe more at tax time.

Do you want a refresher on double trigger RSUs and an example of the tax breakdown? Check out our post What are Double Trigger RSUs and how are they treated?

Should I choose to withhold 22% or 37% in Federal taxes from my IPO vesting?

It depends. How much you withhold for taxes depends on how you want to think about your stock and what your total income for the year will be.

Some individuals view 37% withholding as ‘leaving gains on the table’ for shares that *could have* appreciated. Some individuals view 22% as being a big risk that they may have to sell more shares to cover a tax bill if the stock price goes down.

We encourage you to consider this using examples of what that risk might be for your own situation.

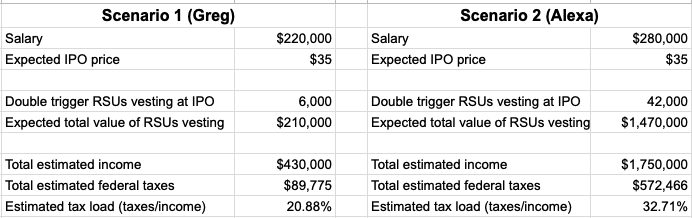

Examples of taxes at an IPO

Let’s choose two situations. The first scenario is for Greg and the second scenario is for Alexa. We assume that both Greg and Alexa have families and are expecting an IPO to happen at year end. This IPO will help them each with buying their next home and getting closer to financial independence. The biggest difference between them is that Greg started at the company as an IC and Alexa came on as a Director. What could their taxes look like?

By estimating what their total income for the year will be and the taxes due, we can get an idea of what their estimated tax load (aka ‘effective tax rate’ may be).

Other considerations for estimating taxes

Some bigger pieces we are leaving out of these examples are:

If your salary is low, chances are your withholding on your salary is much lower than needed at the IPO. Salary withholding tables were made by the IRS assuming your salary is your main income. It matches tax withholding requirements with that income expectation. If both spouses are working, this effect is magnified.

If you have ISOs or NQSOs to consider, the math gets way more complex. We recommend working with your tax advisor or financial planner to create the best strategy for you.

Other sources of income may change the math as well. If you do consulting on the side, have other IPOs in the same year (yes, this has happened to our clients in the past!), or long term rentals, then you will need to up your estimate.

Now let’s see how the 22% and 37% tax withholding election could work out for them.

Examples at 22% tax withholding

This is where total estimated income and the effective tax rate matter. Let’s break down the withholding made a bit further between salary and the RSUs vesting at an IPO.

In this case, the difference in total income makes a huge difference in how much more they will still owe come tax time. Greg may view the risk of $10,000 needed in cash to cover the shortfall as ‘worth the risk’ or up his withholding in case the stock price drops. Alexa’s shortfall could be catastrophic if she isn’t ready to pay $200,000 at tax time.

What are the downsides to taking on the risk of lower tax withholding?

This comes down to what you can afford to take risk wise and what you can’t. Greg may have $10,000+ in cash savings annually and see this as a high risk/high reward worth electing the lower 22% tax withholding for.

Alexa may not have $200,000 laying on the sidelines to pay her taxes with. Even more importantly, what if she did??

Each IPOing employee in this situation should ask themselves:

1. If you sell more for withholding now and it goes up, how would you feel?

2. If you don’t sell enough to cover taxes now and it goes down, how would you feel?

In Alexa’s case, how would she feel paying $200,000 in to cover taxes only to see the stock tumble? If the answer is 🙁, then Alexa should select 37% withholding.

Another consideration is the lockup period. Most IPOing companies have a 180 day lockup period (with some caveats). I don’t have data on how IPOs tend to look 6 months out, but there is a great study at NASDAQ on what happens to IPOs over the long run. Long term, the majority of IPOs do not perform well and drop below their IPO price. This is something to consider in your risk assessment.

Examples at 37% tax withholding

What would happen in each of these scenarios at 37% withholding? Each would end up with a refund after filing their taxes.

I like to think of this as selling some shares at the IPO price – because that is effectively what will happen. 🙂

Through these two examples, you now have an idea of what a 22% tax withholding rate vs 37% tax withholding rate might mean for you. The important thing is that you know what to expect – uncertainty and big tax bill surprises can take the fun out of your Company’s IPO.

Interested in learning more? Sign up for our newsletter

The above discussion is for informational purposes only. Recommendations are of a general nature, not based on knowledge of any individual’s specific needs or circumstances, and there is no intent to provide individual investment advisory, supervisory or management services.