Student loans often begin as a doorway…an investment in possibility, growth, and a future you’re working hard to build. But over time, they can become unnecessarily complex, shifting constantly, and harder to navigate than they should be.

This blog is about understanding how this piece of your financial life fits into the whole of your life, and making decisions that feel steady, informed, and aligned with your goals. Here is how to navigate each stage with clarity.

Before Graduation Day

Your greatest asset in this season is one you might not realize you have: time. A few intentional steps now can reduce friction later and help you step into repayment with more confidence.

- Start with bringing everything into view. Know what you owe, to whom, and under what terms. Federal and private loans are very different, and those differences matter.

- Understand your grace period. For many Federal loans, there’s a six-month window before payments begin. Not all loans follow the same rules, so it’s worth confirming the details.

- If you’re stepping into a new role, look beyond salary. Some employers offer student loan support or retirement matching that can meaningfully shape your strategy.

This time is about preparation and removing uncertainty.

The Grace Period

The first 6 months after graduation is known as: the Grace Period. Similar to when you first started college, these months are often full in more ways than one… new routines, new responsibilities, and a shifting sense of identity. Your loans are present (and accruing interest), but they don’t need to dictate urgency. This is a window to decide how you want to approach them.

Tip: Most servicers offer a 0.25% interest rate reduction for enrolling in automatic payments.

Private Student Loans

Private loans tend to be more rigid. It’s important to understand if the interest rate on your loans is fixed or variable. A fixed interest rate means your payment stays constant over the life of your loan. A variable interest means your payment will fluctuate as interest rates move up and down. Additionally, if you have a co-signer on your loans, it’s important to check your contract for a co-signer release clause. Knowing exactly how many on-time payments are required to remove them can protect your relationships and their credit.

Tip: If rates are high, prioritizing these loans may bring more long-term ease.

Federal Student Loans

Federal loans offer more pathways, but also more complexity. Some plans prioritize consistency with fixed payments, clear timelines, and a defined end point. Other plans prioritize flexibility with payments that adjust with your income, and the possibility of forgiveness over time.

Neither is inherently better. The right choice depends on what matters most to you right now – predictability, flexibility, or a longer-term strategic outcome.

And if public service is part of your path, there are additional opportunities worth understanding early to work towards the 120 month forgiveness goal.

Tip: If you are pursuing loan forgiveness, payments made during your grace period do not count toward loan forgiveness.

Choosing a Repayment Path

So, how do you choose a repayment plan for your Federal student loans? Let’s first review the different repayment plan types.

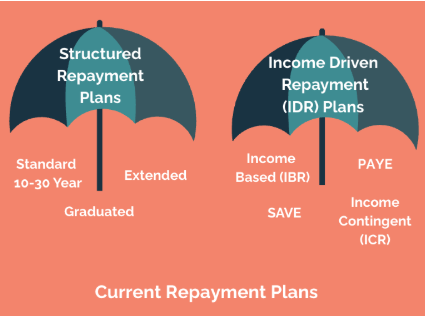

Structured Repayment Plans

Structured Repayment Plans keep a constant payment for a certain period of time. There are 3 types:

- Standard: Loans default to a standard 10 year repayment period. You can increase the repayment period up to 30 years by consolidating your loans. Your monthly payment stays constant over the life of the loan.

- Graduated: Loans default to a 10 year repayment period. You can increase the repayment period up to 30 years by consolidating your loans. Your monthly payment starts low and increases every two years over the life of the loan. If you are starting in an entry-level role, but you expect your salary to jump significantly every few years, this plan matches your payment to your rising career trajectory.

- Extended: You must have over $30,000 in Federal student loans to qualify for this plan. The repayment term is 25 years and you can choose either a fixed payment amount or graduated. If you need to keep your monthly payments as low as possible to afford a mortgage or other life goals, this provides breathing room.

Income-Driven Repayment Plans

Income-Driven repayment plans allow you to keep payments low when income is low while also working towards loan forgiveness over time. To be eligible for the separate Public Service Loan Forgiveness (PSLF) program, you would typically enroll in an Income-Driven repayment plan. All Income-Driven repayment plans calculate your monthly payment based on your Adjusted Gross Income (AGI), NOT your student loan balance.

As of May 15, 2026, there are four different Income Driven Repayment Plans. However, this area is changing quickly, and available options may depend on loan type, borrower status, and implementation timing.

- IBR (Income Based Repayment): Eligible loans include Direct Federal loans, Grad PLUS loans, and FFEL loans. Any unpaid interest on your loan accrues. Loan balances are forgiven after 25 years (if you borrowed before July 1, 2014) and 20 years (if you borrowed on or after July 1, 2014). Any loan balance forgiven is included as taxable income in the year of forgiveness.

- PAYE: Eligible loans include Direct Federal loans and Grad PLUS loans. To be eligible, you cannot have any outstanding loans with a loan date prior to October 1, 2007. Any unpaid interest on your loan accrues. Loan balances are forgiven after 20 years. Any loan balance forgiven is included as taxable income in the year of forgiveness.

- ICR (Income Contingent Repayment): Eligible loans include Direct Federal loans, Grad PLUS loans, and consolidated Parent PLUS loans. Any unpaid interest on your loan accrues. Loan balances are forgiven after 25 years. Any loan balance forgiven is included as taxable income that year.

- SAVE: SAVE is being phased out, and new enrollment is not available. Borrowers currently enrolled should monitor Department of Education and servicer updates before switching plans, because changing plans may affect payment amounts, interest treatment, and forgiveness strategy.

Tip: Federal repayment options are scheduled to change beginning July 1, 2026 for new borrowers. Current borrowers may have different rules depending on their loan type and repayment plan, so confirm available options through StudentAid.gov or your servicer before making changes.

So back to how, do I choose a repayment plan?

Flexibility: If your priority is flexibility, income-driven plans can offer breathing room when income fluctuates and possible loan forgiveness.They ask for ongoing attention since they require annual income and family updates, but in return provide flexibility.

Consistency: If your priority is consistency and simplicity, structured plans offer steady payments, fewer moving parts, and a clear payoff timeline.

Public Service Loan Forgiveness: If you are interested in Public Service Loan Forgiveness (PSLF), you must be enrolled in an Income-Driven Repayment plan and work full-time for an eligible government employer or not-for-profit organization. It’s important to note that PSLF forgiveness is a separate forgiveness path than Income-Driven forgiveness.

The real question isn’t simply what saves the most money. It’s what creates the most stability and alignment for you.

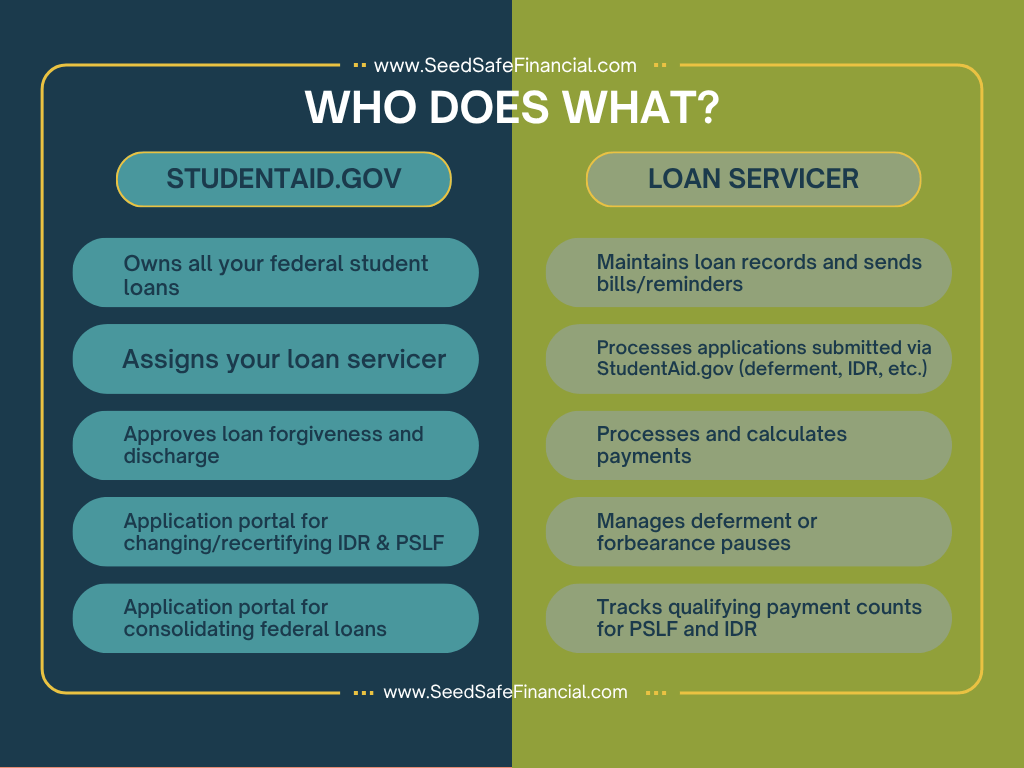

Federal Student Loans: Who Does What?

We are frequently asked between your loan servicer (Mohela, Nelnet, Aidvantage, etc.) and the Federal government (studentaid.gov), who does what? Here is a list of duties for each (although, this is subject to change with the dismantling of the Department of Education):

A common question we receive is about the different roles of your loan servicer (such as Mohela, Nelnet, or Aidvantage) versus the Federal government (via studentaid.gov). Below is a list of duties for each, though keep in mind this is changing with the shifts in the Department of Education.

As Your Life Evolves: Refining the Strategy

A year or two into your career, your relationship with money often shifts. Income grows. Priorities deepen. Life becomes more layered. This is where autopilot is no longer enough and optimization begins.

Private Student Loans

Refinancing private student loans is an ongoing option for lowering your monthly payments. As you build credit and interest rates fluctuate, shopping around for better rates could save you. Since student loan refinancing typically involves no origination fees, it is always worthwhile to compare offers, and you can continue to refinance if lower rates become available in the future.

Federal Student Loans

If you’re on an Income-Driven Plan, you must recertify your income and family size annually. Do not miss this deadline. If you do, your payments may jump back up to the higher Standard Plan amount. If you are married, it may be beneficial to speak with an accountant to determine the trade-off in filing taxes separately if it lowers your student loan payment.

If you qualify for PSLF, submit your Employment Certification Form annually.

If you have extra cash flow, you face a meaningful choice: accelerate repayment or direct those dollars toward investing and other goals

If you qualify, you may be able to deduct up to $2,500 in student loan interest paid on your Federal tax return. This is subject to income phase-outs and, if you are married, you must file Married Filing Jointly.

If refinancing becomes an option, it deserves careful consideration. Lower rates can be attractive, but federal protections, once given up, cannot be regained. Generally, Federal student loans offer greater consumer protection than Private student loans:

- More flexible repayment options

- Forgiveness programs

- Pauses related to deferment or forbearance

- Loan Rehabilitation

- Loan Consolidation

- Loan discharged upon death

There’s no one-size answer here. It’s a decision that lives at the intersection of math and meaning.

A Final Thought

Student loans don’t exist in a static system. Policies change, programs evolve, and what was true a decade ago may not hold today. This doesn’t mean you need to react to every headline, but it does mean your strategy should be revisited as the world shifts around you.

The landscape is currently undergoing one of its most significant transformations in decades. Following the One Big Beautiful Bill Act passed in 2025, we are moving toward a more streamlined, but very different, repayment system starting July 1, 2026.

The goal is to remain steady and responsive. This blog reflects what we know today, but because the guidance is still evolving, we will be posting an update during Summer 2026 as the final rules are implemented. Because repayment-plan availability and forgiveness eligibility, are still being updated, start by verifying your options through StudentAid.gov, your loan servicer, or a qualified advisor before changing repayment plans. The best strategy is to stay informed and proactive. Commit to revisiting your student loan strategy annually to be sure it aligns with your income and goals.

Sources:

Studentaid.gov: Managing Repayment Plans

Student Loan Borrower: Dealing with Student Loan Debt

Congress’ Most Recent Bill on Repayments

Disclaimer:

This material is provided for informational and educational purposes only and does not constitute legal, tax, or investment advice. The strategies discussed may not be appropriate for all individuals or situations. Eligibility and suitability depend on your specific circumstances, financial objectives, and current laws, which are subject to change.

SeedSafe Financial, LLC provides tax preparation and planning services for advisory clients; however, this material is for educational purposes only. Transmission of this information does not create a client-preparer relationship. Please consult with your SeedSafe advisor or a qualified tax professional before implementing these strategies.

Employer plan provisions, contribution limits, and benefits may vary by company. Confirm specific plan details directly with your employer or benefits administrator.

Any examples are hypothetical and provided for illustrative purposes only. They do not represent actual client outcomes, and results will vary. You should consult with qualified tax, legal, and financial professionals before making decisions related to the topics discussed.

References to third-party resources or websites are provided for informational purposes only. SeedSafe Financial, LLC does not endorse or assume responsibility for the accuracy or completeness of external content.

Advisory services are offered through SeedSafe Financial, LLC, an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training.