What is estate planning for young families?

Estate planning for young families protects your family and sets them up for knowing what will happen in an emergency. It defines who will be their guardian, how and when they will receive their inheritance, and what happens if Mom or Dad can’t make decisions.

What are the steps in estate planning for young families?

The best way to create an estate plan is to start with the end in mind.

- Who do you want to take care of your children if you are no longer able to?

- How will your kids be supported as a child vs as a young adult?

- Who is the best steward of your money while the child is growing up?

- How do you want decisions made if you cannot make them for yourself?

- Who is best for project managing your estate through the probate process?

- Are there any mementos or tangible property to leave to someone specifically?

- Who can keep the ship running financially if you mentally cannot while you are living?

- What will happen to any pets after you pass?

Then, with these questions answered, you are ready to learn more about the different pieces of an ‘estate plan’.

What should you include in an estate plan for young families?

Will: This document outlines your wishes of who should get your assets, who will be the Guardian of your kids, and who can take this information through the probate process (i.e. Executor)

Financial Power of Attorney: A power of attorney allows you to appoint someone you trust to make financial decisions for you when you cannot (i.e. if you are incapacitated)

Medical Power of Attorney (Healthcare Directive): A healthcare directive allows you to appoint someone you trust to communicate your medical and end-of-life wishes. This person may be the one to say ‘pull the plug’, so make sure they are okay being in charge

Trust: The main reasons we like a trust are for privacy, potential tax advantages, and for a more intentional plan on when your children receive money. If you have over $500,000 in assets, ask yourself: Do I feel comfortable with my child receiving $500,000+ at age 18 with no restrictions? What do I hope they can accomplish with the money? Then, you can structure a trust to best align with your wishes

Beneficiary designations: Not everything goes through a Will. If you have retirement accounts (i.e. 401(k)s and IRAs) then the accounts will go to any listed beneficiaries. Review this to make sure it is inline with your wishes

Emergency letter: The majority of an estate plan are legal documents saying who and what, but an emergency letter is a way of saying how. This can give your family a wonderful head start in contacts for help and the ins and outs of your monthly cash flow now. We recommend putting this in place and keeping it up to date

Communication: Make sure the people involved in your estate plan have the documents they need to start acting in an emergency. If they don’t have access, then it will make the transition harder and not give your family the support you need when something happens

How does an estate plan work?

At the basic level, an estate plan is taken through the probate process. Probate is a fancy word for a public legal process with the county court for validating the will, notifying creditors, settling debts and taxes, and distributing the remainder to beneficiaries. Even if you do not have a will, there will still be a plan – the state’s plan for who should receive your money. Proper estate planning helps minimize these issues and a Trust can help you keep more of the money details private.

Part of the probate process is wrapping up tax returns. The current Federal estate tax exemption is around $11.2 million per person, and that is set to ‘sunset’ in 2025 back to the pre-TCJA Act exemption level. This would be somewhere around $7 million per person in 2025. Your goal for using trusts vs. just a will may differ if you are under or over the exemption level.

Estate planning and state estate taxes

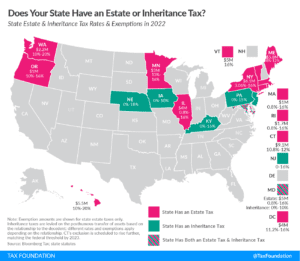

State estate taxes are something many individuals forget about. These can impact how much your beneficiaries may take home. Some states call this an ‘estate tax’ while others may consider it an ‘inheritance tax’. The Tax Foundation offers a wonderful overview of which states are impacted.

You may find more information on the above chart from the Tax Foundation HERE.

In the end, the process may take a while to wrap up. So the more detail we can provide on where things are and our wishes, the better. Don’t leave your family scrambling to understand how to move forward while they are already emotionally drained from losing you.

Estate plans need routine check-ins

Estate planning for young families is about peace of mind. Peace of mind that your wishes are known and being upheld. Peace of mind for your family on how to help unwind everything. We believe clarifying and streamlining this process will help keep you safe and allow your family the best path forward.

Remember, this is not a ‘one and done’ process. Life changes over time and so should your estate plan. As you reach new financial milestones and your family evolves, we recommend reviewing your estate plan to ensure it continues to evolve as you do.

We recommend working with your financial advisor and attorney to make sure your estate plan is kept up to date and brought forward for review when tax regulations change or new policies arise.

Interested in learning more? Sign up for our newsletter

The above discussion is for informational purposes only. Recommendations are of a general nature, not based on knowledge of any individual’s specific needs or circumstances, and there is no intent to provide individual investment advisory, supervisory or management services.